In today’s economic climate, many individuals find themselves struggling to keep up with mounting credit card debt.

When the bills pile up and minimum payments become a challenge, some may consider simply stopping their credit card payments altogether. However, this decision can have serious and far-reaching consequences.

Let’s explore what can happen when you stop paying your credit cards and why seeking professional debt relief services may be a smarter alternative.

The Domino Effect of Missed Payments

When you miss a credit card payment, it sets off a chain reaction that can quickly spiral out of control:

Late Fees and Penalties

Credit card companies typically charge late fees ranging from $25 to $40 for each missed payment. These fees add up quickly, increasing your overall debt.

For example, if you have three credit cards and miss a payment on each, you could be looking at up to $120 in late fees for just one month. Over the course of a year, this could amount to over $1,400 in late fees alone. Some cards may also have penalty APRs that kick in after a missed payment, which can be as high as 29.99%.

Interest Rate Hikes:

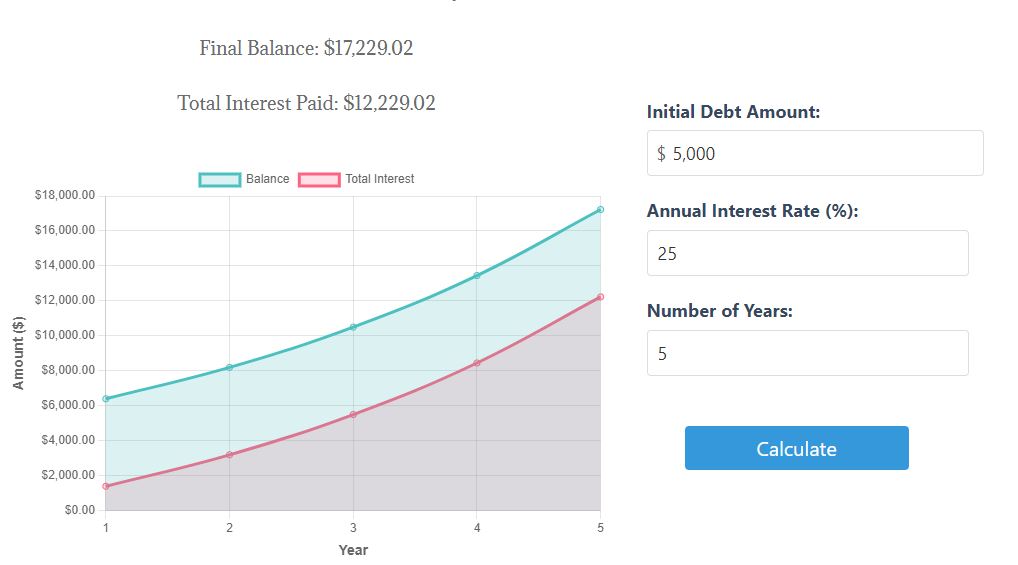

Many credit card agreements include a clause allowing the issuer to raise your interest rate if you miss payments. This can dramatically increase the amount of interest you owe each month. Using our Total Paid Interest Calculator tool, you can see how this interest rate hikes can ruin your financial security.

For instance, if you have a $5,000 balance on a card with a 15% APR, and your rate jumps to 25% after a missed payment, your annual interest charges would increase from $750 to $1,250.

This $500 increase means you’re paying more in interest and less towards your principal balance, extending the time it takes to pay off your debt.

Damage to Your Credit Score

Payment history is the most significant factor in determining your credit score, accounting for about 35% of your FICO score. Even a single missed payment can cause your score to drop by 50 to 100 points or more.

For example, someone with a good credit score of 780 might see their score plummet to 680 after a 30-day late payment. This drop could move them from the “very good” credit category to merely “fair,” potentially affecting their ability to secure loans, rent apartments, or even get certain jobs.

Calls from Debt Collectors

After 30 days of non-payment, your account may be turned over to a collection agency. This can lead to frequent, stressful phone calls and letters demanding payment.

Debt collectors are known for their persistent tactics. They may call you at home, at work, or contact your relatives to try to locate you. While there are laws regulating debt collection practices (such as the Fair Debt Collection Practices Act), the experience can still be incredibly stressful and disruptive to your daily life.

Legal Action

If you continue to ignore your debt, the credit card company may sue you to recover what you owe. This can result in wage garnishment or liens on your property.

For example, if a creditor wins a judgment against you, they might be able to garnish up to 25% of your disposable earnings. On a $3,000 monthly salary, this could mean losing $750 each month to debt repayment. Additionally, a lien on your property could prevent you from selling your home or car without first paying off the debt.

Long-Term Financial Impact

A damaged credit score can affect your ability to rent an apartment, secure a mortgage, or even get certain jobs. The effects can last for years, making it difficult to rebuild your financial life.

For instance, a missed payment can stay on your credit report for up to 7 years. During this time, you might face higher interest rates on any loans you do qualify for, larger security deposits for rentals or utilities, and potentially missed job opportunities if employers check credit as part of their hiring process.

A person with poor credit might pay $50,000 more in interest over the life of a 30-year mortgage compared to someone with excellent credit.

The Snowball of Debt

As these consequences pile up, your original debt can quickly balloon out of control. Late fees, higher interest rates, and legal costs can turn a manageable debt into an insurmountable financial burden. What started as a temporary solution to financial stress can become a long-term nightmare.

If you know you’re going to fail paying your credit cards or haven’t made a payment for a while and waiting for the consequences, don’t wait anymore and contact Alesure team.